Summer 2022 Newsletter

Is there opportunity in market volatility?

When markets are volatile, everyone’s pleased with the upswings, perhaps eagerly checking out their portfolio balance. But the downswings can be another story. Maybe those portfolio balances still get checked, but nervously.

Silver linings

Fortunately, during the wealth accumulation years, market downturns can bring opportunity. When share prices fall, the money managers behind your investments see prospects for profit. They can add to current holdings at discounted prices or invest in companies on their watch list that were previously too expensive.

Just as money managers can take advantage of buying low, so too can investors. All you need to do is continue making regularly scheduled contributions, even when markets are down. Sometimes it may take patience and discipline, but when markets recover and stock prices rise, the money managers’ individual stock picks and your continued investments can boost your portfolio’s value. It’s a buying opportunity.

When to manage volatility

Market volatility doesn’t always have a silver lining. When approaching retirement, you don’t want to risk a significant market downturn that might cause you to postpone your retirement date. So most investors typically make their investments more conservative to help preserve their portfolio as retirement nears.

During retirement, market downturns certainly don’t represent buying opportunities – since you’re now drawing income, not investing new money. Several strategies are available to minimize the effects of market volatility, including holding investments in stable companies historically less volatile and drawing retirement income from a cash reserve that allows time for any downtrodden equity investments to recover.

Talk to us if volatile markets, particularly the downswings, ever cause you to worry. We can discuss investment opportunities and also make sure your portfolio remains aligned with your risk tolerance.

Investing

Why diversification matters

Investing can be unpredictable. Will interest rates remain the same, go up or fall – and when? Exactly where are we in the market cycle, and how long until we enter the next phase? Will a geopolitical event, health crisis or other incident shock the markets? Which investments offer the most opportunity over the next year?

Everyone can try to make predictions, but no one can always know the answers. That’s one of the key factors behind the strategy of creating a fully diversified portfolio. Since we can’t predict the market leaders or underperformers year to year, it’s best to cover all bases.

Benefits of diversification

A well-diversified portfolio can benefit investors in three key ways.

- Minimize risk. By spreading your investment dollars across a variety of investments, you ensure that you won’t be over-invested in any particular underperforming market.

- Enhance performance. Every January, investment analysts predict which markets will be among the year’s leaders, and invariably every December we’re reminded to expect the unexpected. However, if your investments are fully diversified, you will likely have some exposure to the year’s market leaders, which can potentially enhance portfolio returns.

- Reduce volatility. If a portfolio only includes a handful of investments that respond alike to the same economic conditions, portfolio returns could rise and fall sharply at the whim of the markets. A fully diversified portfolio is constructed with investments that react differently to economic conditions, which smooths out returns and reduces portfolio volatility over time.

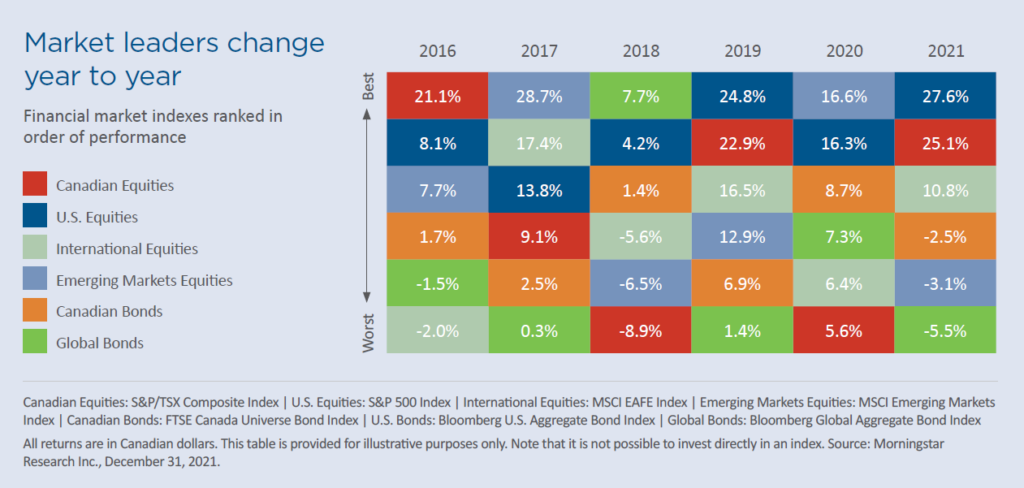

A look at market indexes

Talking about portfolio diversification in theory is instructive, but the benefits are much clearer and more impactful when you view market unpredictability in reality. Take a look at the table below to note the following observations.

The notion that an investment can go from laggard to leader in just one year is demonstrated by Global Bonds. In 2017, they sit at the very bottom rank, then in 2018 Global Bonds rise to market leader.

To see how any investment can be unpredictable year to year, follow Canadian Equities from left to right to track a zig-zag path that hops up, down and in between.

By diversifying, you have a greater chance of gaining exposure to the best-performing markets. In just the six years represented on this table, four different indexes held the position of market leader.

Ways to diversify

The broadest way to diversify an investment portfolio is through investing in different asset classes, the major ones being equities, fixed income and cash equivalents. You can also be diversified within each asset class. For example, within equities, you can be invested in small-cap, mid-cap and large-cap companies – “cap” or capitalization referring to a company’s size.

Investment style offers another way to diversify, as value and growth investments often take turns outperforming each other. Investing in a variety of geographic regions also provides all the benefits of diversification – and opens up specific investment opportunities less available in Canada.

If you would like to talk about the various ways your investments are diversified, please get in touch.

Retirement Planning

Should you and your spouse retire together?

It may seem natural and expected for a couple to have the same retirement date, starting this new chapter of their life together. But it’s quite common for spouses to retire at different times.

Personal reasons for retiring apart

An age gap of several years or more is behind a great many couples’ decision for one spouse to retire before the other. But a variety of situations can lead to retiring at different times. One spouse may retire earlier than planned due to ill health. Or a spouse may leave their job to look after an elderly parent who needs care. Perhaps one spouse receives an early retirement offer from their employer. Or one spouse might work past the traditional retirement age because they find their work fulfilling, while the other spouse looks forward to retirement.

The financial factor

The decision of whether or not to retire at the same time often involves a financial factor. Take the situation of a couple with an age gap. Say one spouse is 65 and the other is 60. They’re thinking about both retiring now, so they’ll have more of their younger years to enjoy retirement together. However, if the older spouse retires now, and the younger spouse works for a few more years, the additional savings may give the couple a more comfortable retirement lifestyle. Also, while the younger spouse receives income, the retired spouse can possibly delay withdrawals from retirement savings.

How does this couple decide? It can be a lot easier when you involve us with the financial side of the decision. We can show you what your estimated level of retirement income and overall financial picture could be with a staggered retirement and a synchronized retirement. Then you can consider both the personal and financial factors to make an informed decision.

Education Planning

Managing asset allocation in an RESP

A Registered Education Savings Plan (RESP) has three important phases where the asset allocation between equities, fixed income and cash equivalents is critically important.

Initial years

If an RESP is opened fairly soon after a child’s birth, the long time horizon allows for a heavy focus on equities for greater potential returns. Starting a plan with 75% or more in equities is quite common. But equally important is the risk tolerance of the person who opens the RESP, known as the subscriber. An aggressive investor might start with 90% of their plan in equities, whereas a conservative subscriber may start with 75% in fixed income, and the plan chosen could be perfectly suitable for each person.

The conservative investor, like all subscribers, can still take full advantage of the Canada Education Savings Grant (CESG). The first $2,500 of annual contributions triggers $500 in grant money, to a maximum of $7,200 for each beneficiary.

Middle years

Whatever the initial asset allocation happens to be, it’s common for subscribers to gradually reduce equities and increase fixed-income investments to some degree during the middle years of an RESP. It’s all about protecting your investments from the risk of a significant or prolonged market downturn when there is not enough time remaining for the markets and RESP to recover and grow. To illustrate, some subscribers with a moderate risk tolerance might have an RESP that’s approximately 50% equities and 50% fixed income when the child is about 8 to 10 years old.

Approaching graduation

Different subscribers’ asset allocations may vary greatly in the early years, but they’ll typically be quite similar by the time secondary school graduation nears. In these final years, equities are reduced, sometimes to zero. Fixed-income investments increase and cash equivalents are introduced. For many subscribers, the entire plan may be invested in cash and low-risk investments before it’s time to withdraw funds for tuition and expenses.

Financial briefs

Should you invest in cryptocurrency?

The first cryptocurrency, Bitcoin, was designed as a digital currency to make and receive payments exclusively online, without involving a financial institution. Today, there are thousands of cryptocurrencies – but they’ve become more of an investment phenomenon than a usable currency.

As an investment, cryptocurrency has been extremely volatile. For example, there have been periods in the past couple of years when you could have tripled a Bitcoin investment in 12 months or lost half the value of your investment in three months.

Investors can buy a specific cryptocurrency from an online exchange or trading platform, or invest through a cryptocurrency mutual fund or exchange-traded fund (ETF).

Speculators aim to benefit from the large swings by buying low and selling high. Long-term investors are willing to ride out the volatility, expecting their investment to trend upward over time.

As a high-risk asset class, cryptocurrency is not for every investor. If you do want to learn more about cryptocurrency as an investment, please get in touch.

What to do after you pay off your mortgage

It’s a significant milestone when you make that final mortgage payment. Now you have a sizable amount of extra funds to use as you wish. The question is, what’s the best way to apply this new cash flow?

For many people, the prudent decision is to allocate the funds to retirement savings. This choice can either allow you to retire earlier or spend your retirement more comfortably.

But you might have other goals in mind. The money could help fund a child’s or grandchild’s education, or go toward an adult child’s down payment on their first home. You could make home or vacation property renovations, fund a vacation, pay for a second car or bolster an emergency fund.

In many cases, our services can help you with choosing your goal. For example, a couple may want to confirm their retirement savings are on track before funding their child’s down payment. We’re here to assist you with the financial side of your decision.

Preparing an estate directory

Imagine if an estate executor (or personal representative, liquidator or estate trustee, depending on the province) was about to administer an estate, only having the will. They would have a tough time searching for contact people, important documents and hidden information. That’s why it’s important to develop an estate directory including everything your executor needs.

Start with the contact information of your lawyer, accountant, advisor and beneficiaries. State the location of your will, insurance policies, tax returns and safety deposit box. Provide bank account information. List assets, including registered plans and investment accounts, real estate and valuable items. Also, list debts, whether credit cards, a mortgage, loan or line of credit. This is not even a complete list, so imagine the complex ordeal an executor would face without this help.

Please feel free to contact us about the information an estate directory should include. If you’ve already prepared a directory, it’s a good idea to review it periodically, and make updates when required.

This newsletter has been written (unless otherwise indicated) and produced by Jackson Advisor Marketing. © 2022 Jackson Advisor Marketing. This newsletter is copyright; its reproduction in whole or in part by any means without the written consent of the copyright owner is forbidden. This is not an official publication of iA Private Wealth and the information in this newsletter does not necessarily reflect the opinion of iA Private Wealth Inc. The information and opinions contained in this newsletter are obtained from various sources and believed to be reliable, but their accuracy or reliability cannot be guaranteed. The opinions expressed are based on an analysis and interpretation dating from the type of publication and are subject to change. Furthermore, they do not constitute an offer or solicitation to buy or sell any of the securities mentioned. The information contained herein may not apply to all types of investors. Readers are urged to obtain professional advice before

acting on the basis of material contained in this newsletter.

Mutual funds are not guaranteed and information on returns is based on past performance which may not reflect future performance. Mutual funds may be associated with commissions, trailer fees, management fees and other expenses. Please read the prospectus. Important information regarding mutual funds may be found in the simplified prospectus. To obtain a copy, please contact your Investment Advisor.

iA Private Wealth is a trademark and business name under which iA Private Wealth Inc. operates. iA Private Wealth Inc. is a member of the Canadian Investor Protection Fund and the Investment Industry Regulatory Organization of Canada. Only products and services offered through iA Private Wealth Inc. are covered by the Canadian Investment Protection Fund.

Posted In: PostsNewsletter